Short summary

Mergers and acquisitions are often promoted as engines of growth, promising efficiency gains and stronger, more competitive firms. Yet they can also eliminate rivals and reshape markets. This is why antitrust policy has traditionally focused on weighing potential benefits against risks to consumers. Much less attention has been paid to what acquisitions mean for workers.

Using data from Sweden, this study finds that firms that take over others do initially expand as they absorb their targets. Looking at the two firms together, however, a different picture emerges. The combined business ends up employing fewer workers and generating less revenue in the years after the acquisition, compared with similar pairs of firms that were not involved in a takeover. Profits across the combined firms decline as well.

Workers bear much of the cost. Employees at both acquiring and target firms experience large and persistent earnings losses relative to similar workers elsewhere. Many lose their jobs or move to smaller, lower-paying firms. Even those who remain employed often see slower wage growth. Especially in cases where the acquisition increases profits at the acquiring firm.

Key Findings

- Acquiring firms grow sharply at first, then scale back. Employment and revenue jump after the acquisition, then decline over time. Five years later, employment is 20 percent higher and revenue 5 percent higher than comparable non-acquiring firms.

- The combined firm shrinks. Employment across the acquiring and target firms is about 30 percent lower five years after the acquisition than in similar firm pairs that were not involved in a takeover, and revenue around 40 percent lower.

- Workers experience large and lasting earnings losses. Relative to comparable workers, those employed at acquiring and target firms earn about 9 percent less in the fifth year after an acquisition.

- Most losses come from job displacement. Roughly four-fifths of the average relative earnings decline results from job separations. The remaining losses come from slower wage growth among workers who stay.

- Wage growth slows even when acquisitions are profitable. Workers who remain often see wage growth reduced, especially in cases when profits rise after the deal.

Author Quote

“Many acquisitions are followed by layoffs and lower earnings for workers, and even those who remain employed often see slower wage growth.”

Reference: Based on RFBerlin Discussion Paper No. 76/25, Beuschlein, Sigurdsson, and Wong (2025) The Labor Market Consequences of Acquisitions.

Research summary

The big picture

Corporate takeovers are usually presented as a way to improve firm performance, through cost cutting, reorganization, or the combination of complementary activities. Whether such changes actually deliver lasting gains for the firms involved is an empirical question. What they mean for the workers employed by them is another.

Using data from Sweden covering the period from 1997 to 2018, this study shows that the answer is unambiguous: workers lose. Acquiring firms do grow after a takeover, expanding employment and revenue relative to similar firms that did not make an acquisition. But this expansion fades over time. When the acquiring and target firms are considered together, employment, revenue, and profits all decline relative to comparable firm pairs that were not involved in a takeover. These firm-level changes translate into lasting losses for workers, through both job displacement and slower wage growth among those who stay.

Why does wage growth slow? One common explanation is that acquisitions reduce workers’ outside options, allowing firms to exert greater bargaining power over pay. If firms competing for the same workers merge, employees may find it harder to switch jobs and negotiate higher wages. While this story seems plausible on paper, the data tell a different story.

Instead, most of the decline in wage growth is driven by a subset of acquisitions. These account for roughly three quarters of the total and involve managers from the acquiring firm already held a seat on the target firm’s board. These insider managers tend to acquire firms that paid above-market wages. This makes it easier to slow wage growth of workers previously employed at the target firm after the acquisition. Following such acquisitions, profits at the acquiring firm tend to rise even as workers’ pay falls behind. Taken together, the results are consistent with a redistribution of rents away from workers, rather than productivity gains that are shared more broadly.

Consequences for Firms and Workers

The study compares workers and firms involved in an acquisition with similar workers and firms that will not be acquired until several years later. This allows the analysis to separate the effects of the takeover from broader trends affecting firms and workers over time.

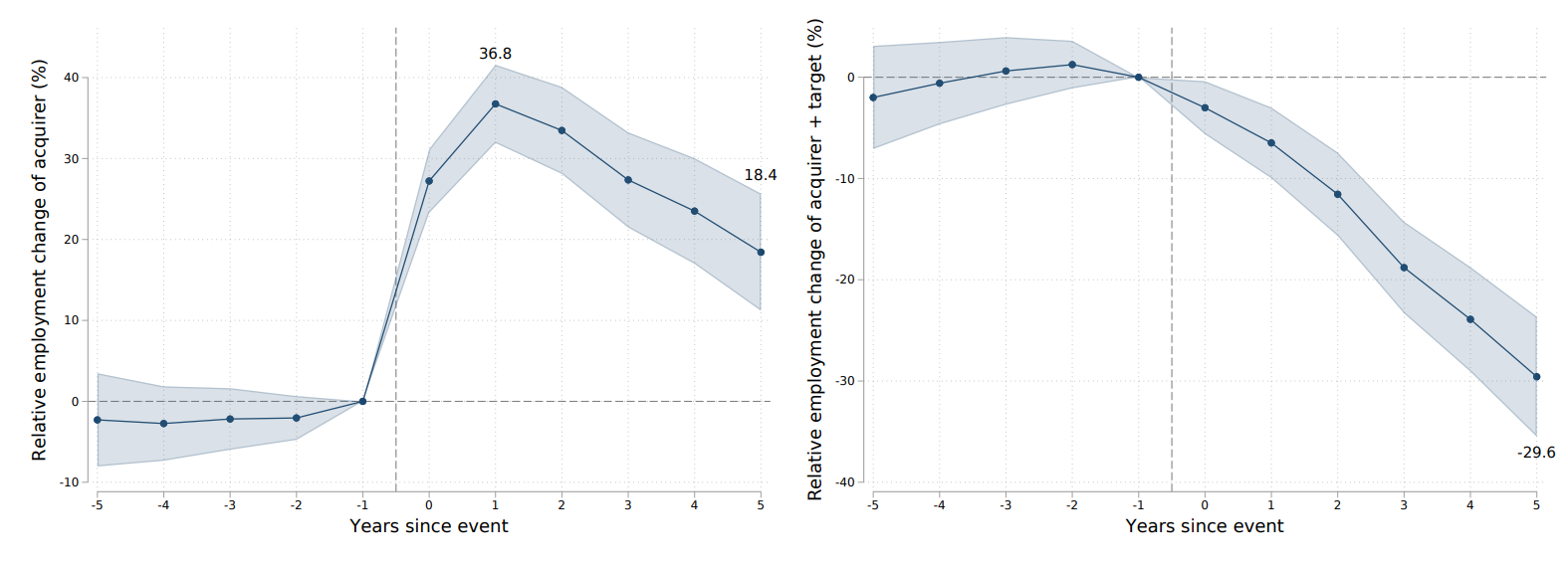

Figure 1 shows how firm employment evolves before and after an acquisition. Shortly after the takeover, employment at the acquiring firm rises sharply, by about 37 percent compared to the control group, reflecting the absorption of the target (Figure 1a). This initial expansion gradually unwinds over time, but five years after the deal the acquiring firm remains 18 percent larger than comparable non-acquiring firms. Revenue at the acquiring firm follows a similar pattern. It rises at the time of the acquisition and then partially declines and is about 5 percent higher than at comparable firms five years later. By contrast, profits at the acquiring firm evolve similarly to those at comparable firms, with no relative increase following the acquisition.

When the acquiring and target firms are considered together, a different pattern emerges. Both employment and revenue at the combined firm decline following the acquisition. Five years later, total employment across the combined firm is around 30 percent lower than for similar firm pairs that were not involved in a takeover (Figure 1b), and combined revenue is about 40 percent lower. Profits across the combined firm also fall, by roughly 30 percent. In the long run, acquisitions show little sign of improving firms’ overall performance.

Figure 1a (left), Figure 1b (right)

Notes: This figure shows average employment changes of firms undergoing an acquisition relative to comparable firms undergoing an acquisition 7 years later. Changes are measured in percent relative to the year prior to the acquisition. Panel (a) shows the outcome of the acquiring firm only, and panel (b) shows total employment of the acquiring and target firm combined. Shaded areas indicate 95 percent confidence intervals, illustrating statistical uncertainty of the estimates.

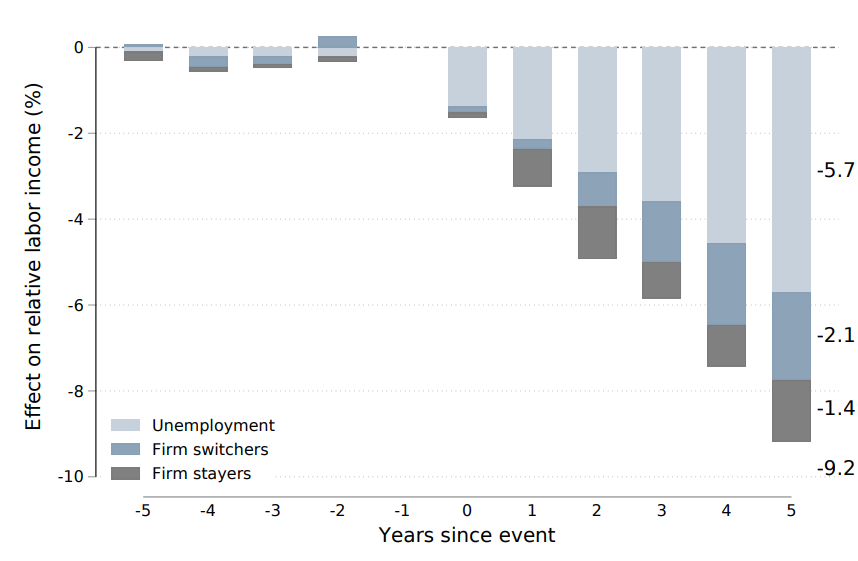

Figure 2 shows how acquisitions affect workers’ earnings in the years before and after the takeover, focusing on employees aged 23 to 60. Relative to comparable workers, labor income falls persistently following an acquisition. On average, annual earnings decline by about 5 percent throughout the post-acquisition period and reach a decline of 9 percent five years after the deal.

The majority of these losses are driven by job displacement. Transitions into unemployment account for the largest share of the earnings decline, with older and less educated workers particularly affected. A further substantial share comes from workers who leave for other firms, which tend to be smaller, pay lower wages, and offer worse jobs than the firms they leave. A smaller but still meaningful portion of the overall loss reflects slower wage growth among workers who remain employed at the acquiring firm.

Figure 2

Notes: This figure reports the average change of workers’ labor market income around the time of an acquisition, relative to comparable workers who undergo an acquisition seven years later. Changes are expressed as percent, relative to the year prior to the acquisition. The total effect is composed into three distinct channels: transitions into unemployment, moves to other firms, and changes for workers who remain at the firm.

Lower wage growth is driven by insider acquisitions

Given the firm-level results, job losses following acquisitions are not hard to understand. When firms shrink or fail to grow, layoffs and worker reallocation naturally follow. What is more difficult to explain is why wage growth slows even for workers who keep their jobs.

Recent discussions among policymakers and academics have raised concerns that mergers and acquisitions may contribute to slower wage growth by weakening competition in labor markets (see, e.g. Prager, 2026). The idea mirrors a familiar concern from product markets. When firms gain monopoly power, they can raise prices and harm consumers. Similar forces can operate in labor markets. When firms that compete for the same pool of workers merge, employees may find it harder to switch jobs or use outside offers to negotiate higher pay. Economists refer to this form of employer market power as monopsony. Despite these concerns, the wage declines observed here do not appear to be driven by increases in firms’ monopsony power after acquisitions.

The study examines this idea in two ways. First, most acquisitions do not take place between firms that previously hired from the same pool of workers. Hence the takeovers arguably do not reduce workers’ outside options. And even when the firms previously directly competed, wage growth does not fall more than in other acquisitions. Second, the analysis asks whether wage effects are stronger when an acquisition substantially increases the combined firm’s presence in a local labor market, defined by occupation and municipality. Acquiring a large employer should, in principle, give a firm more leverage over workers than acquiring a small one. Yet wage growth declines by a similar amount regardless of whether the target firm accounts for a large or a small share of local labor market employment.

Instead, the evidence is consistent with a different story. Firms may already have the ability to restrain wages, but they do not always choose to do so. Managers may not cut pay, unaware of how far wages could be pushed down, or constrained by implicit understandings with their workforce. As a result, some firms continue to pay wages that are high relative to what market conditions alone would sustain. This leaves scope for outside acquirers to step in and alter pay-setting practices after a takeover.

This mechanism becomes visible once acquisitions are separated by whether senior managers of the acquiring firm already had prior involvement with the target firm. In these insider acquisitions, a senior executive of the acquiring firm had previously served on the target firm’s board, giving them detailed knowledge of its finances and pay structure. Among workers who remain employed after the takeover, wage growth declines most sharply for those previously employed at the target firm. By contrast, when no such insider connection exists, wage growth for remaining workers is largely unchanged. Consistent with this pattern, acquiring executives are more likely to target firms where workers earned relatively high wages before the takeover, suggesting that insider access helps identify scope for post-acquisition wage restraint.

Following such insider acquisitions, total employment and revenue across the combined firm remain roughly stable, while profits on the acquirer’s side increase, along with CEO compensation. Lower wages among target-firm employees account for about one-third of this profit increase. Taken together, the evidence suggests that insider acquisitions are motivated less by productivity gains and more by opportunities to shift existing rents from workers to executives and shareholders.

References

- Acemoglu, D., A. He, and D. Le Maire (2023): “Eclipse of Rent-Sharing: The Effects of Managers’ Business Education on Wages and the Labor Share in the US and Denmark,” Working paper.

- Arnold, D. (2021): “Mergers and Acquisitions, Local Labor Market Concentration, and Worker Outcomes,” Working paper.

- Arnold, D., K. Milligan, T. Moon, and A. Tavakoli (2024): “Job Transitions and Employee Earnings After Acquisitions: Linking Corporate and Worker Outcomes,” Working paper.

- Lagaras, S. (2024): “M&As, Employee Costs and Labor Reallocation,” Journal of Finance

- Prager, E. (2026): “Antitrust Enforcement in Labor Markets,” Journal of Economic Perspectives, 40(1), pp. 115-138.

Disclaimer

The opinions and views expressed in this publication are those of the author(s) and do not necessarily reflect those of the ROCKWOOL Foundation Berlin (RFBerlin). While research disseminated through this series may address policy-relevant topics, RFBerlin, as an independent research institute, does not take institutional policy positions.

Publications in the RFBerlin Research Insights series may represent preliminary or ongoing work that has not been peer-reviewed. Readers are advised to consider the provisional nature of such research when citing or applying its findings.

These publications aim to make scientific work accessible to a broader audience and to encourage informed, research-based discussion. All materials are provided by the respective authors, who bear responsibility for appropriate attribution and rights clearance. While every effort has been made to ensure accuracy and proper acknowledgment, RFBerlin welcomes notifications of any concerns regarding authorship, citation, or intellectual property rights. Please contact RFBerlin to request corrections if needed.

Use of these materials for the development or training of artificial intelligence systems is strictly prohibited.