Summary

- After more than a decade of sustained growth, the number of refugees and asylum-seekers in the EU27 and the UK stabilised in 2025 at 9.6 million, virtually unchanged from 2024 (+0.1%) after rising 6.3% the year before.

- The stable total conceals a shift in composition: the Ukrainian population held at 4.6 million (48% of the total) and the Syrian population fell by 7%, while the number of Venezuelans rose by 26%.

- The aggregate stability masks offsetting movements across host countries: Germany declined for the first time in more than a decade (-4.7% to 2.95 million), as did Poland (-1.5%) and Italy fell sharply (-17.9%), while France (+7.8%), Spain (+9.6%) and the United Kingdom (+13.3%) continued to grow.

- New asylum applications fell for a second consecutive year, by 23.8% to 770,000. The application decline is concentrated in a few origins. In particular, Syrian claims collapsed by more than 70%.

- Germany’s decline reflects primarily naturalisations, rather than returns: for Syrians and Iraqis (accounting for 61% of the non-Ukrainian fall), naturalisation explains most of the decrease, while assisted returns are small.

Stabilisation of the Refugee and Asylum Seekers Population

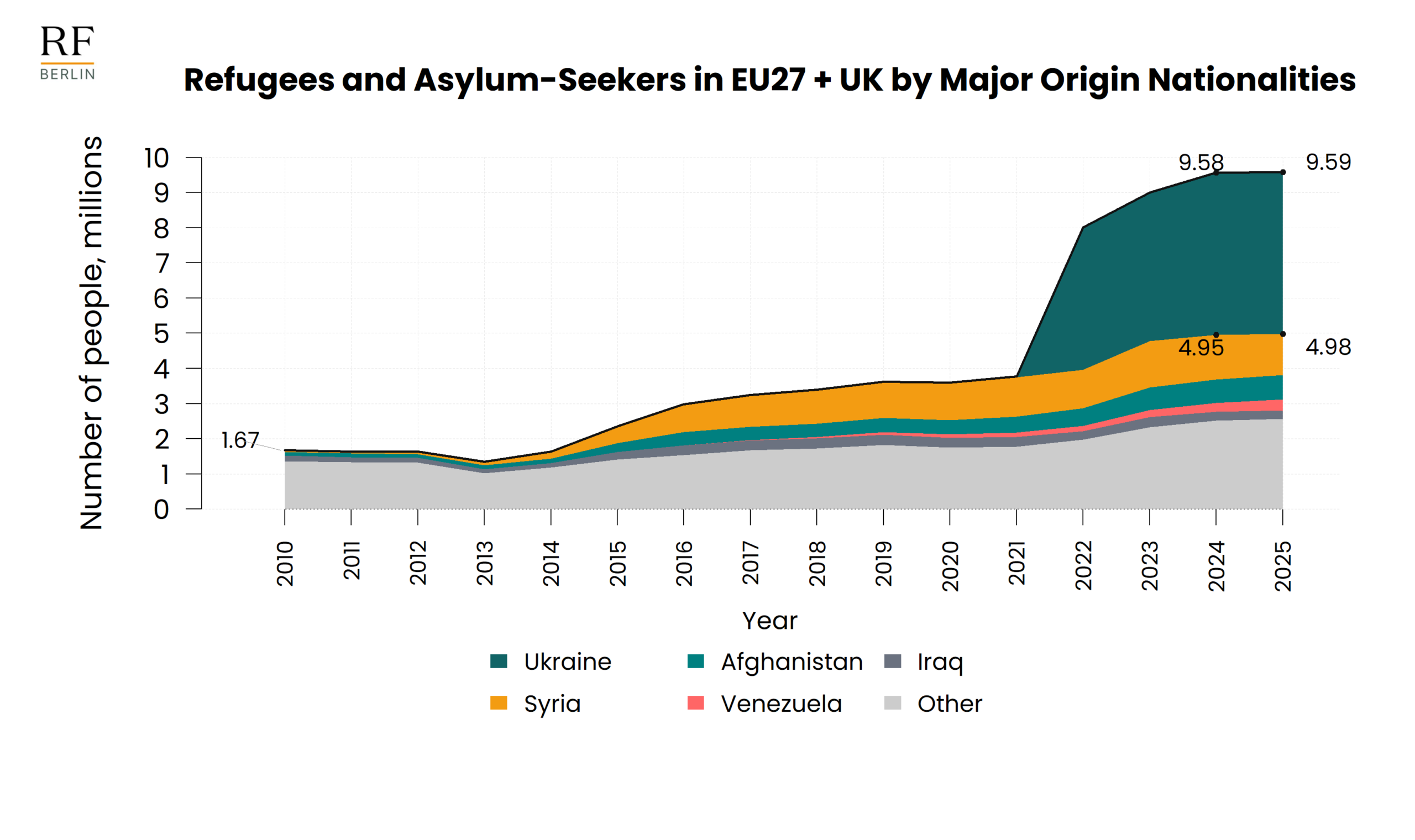

Europe’s refugee population remains at a historically high level, with the combined number of refugees and asylum-seekers rising from 1.7 million in 2010 to 9.6 million in 2025, driven first by displacement from Syria and later by the large-scale arrival of people fleeing Russia’s invasion of Ukraine. Ukrainians now constitute the largest refugee population in Europe, accounting for 4.6 million people, while Germany remains by far the largest host country with nearly 3 million refugees and asylum-seekers. At the same time, the rapid expansion observed after 2022 has largely come to an end. Total refugee and asylum-seeker stocks were essentially unchanged between 2024 and 2025.

Between 2010 and 2025 the combined number of refugees and asylum-seekers in the EU27 and the UK rose more than five-fold, from 1.7 million to 9.6 million. This number includes also individuals in refugee-like situations like holders of temporary protected status. As Figure 1 shows, the total grew gradually through the 2010s, reaching roughly 3.6 million by 2019 in the wake of the Syrian crisis. The steep increase after 2022 was driven almost entirely by displacement from Ukraine, which accounted for 4.6 million people, or 48% of the total, in 2025.[1]

The 2025 data indicate that this expansion has come to a halt: the total was virtually unchanged from 2024 (+0.1%), after growing by 6.3% the year before. Beneath the stable aggregate, the composition continued to evolve. The Ukrainian population levelled off, and the Syrian declined by 7.2%, to 1.18 million, while the number of Venezuelans rose by 26%, to roughly 308,000, and the Iraqi population contracted by 10%. Taken together, these shifts suggest that the acute, crisis-driven phase of growth has passed and that the population is increasingly shaped by more gradual and diverse inflows. A substantial “Other” category (2.57 million, or 27% of the total) underscores that displacement to Europe draws on a broad set of origins beyond the headline crises.

Figure 1

Source: UNHCR, (downloaded on 11 June 2026). Notes: End-year number of refugees and asylum-seekers in the EU27 and the UK, 2010–2025. Refugees include individuals granted refugee status, complementary protection, temporary protection, and persons in refugee-like situations. Asylum-seekers are individuals whose asylum claims have not yet been finally decided. The temporary decline in 2013 reflects a change in Germany’s reporting methodology.

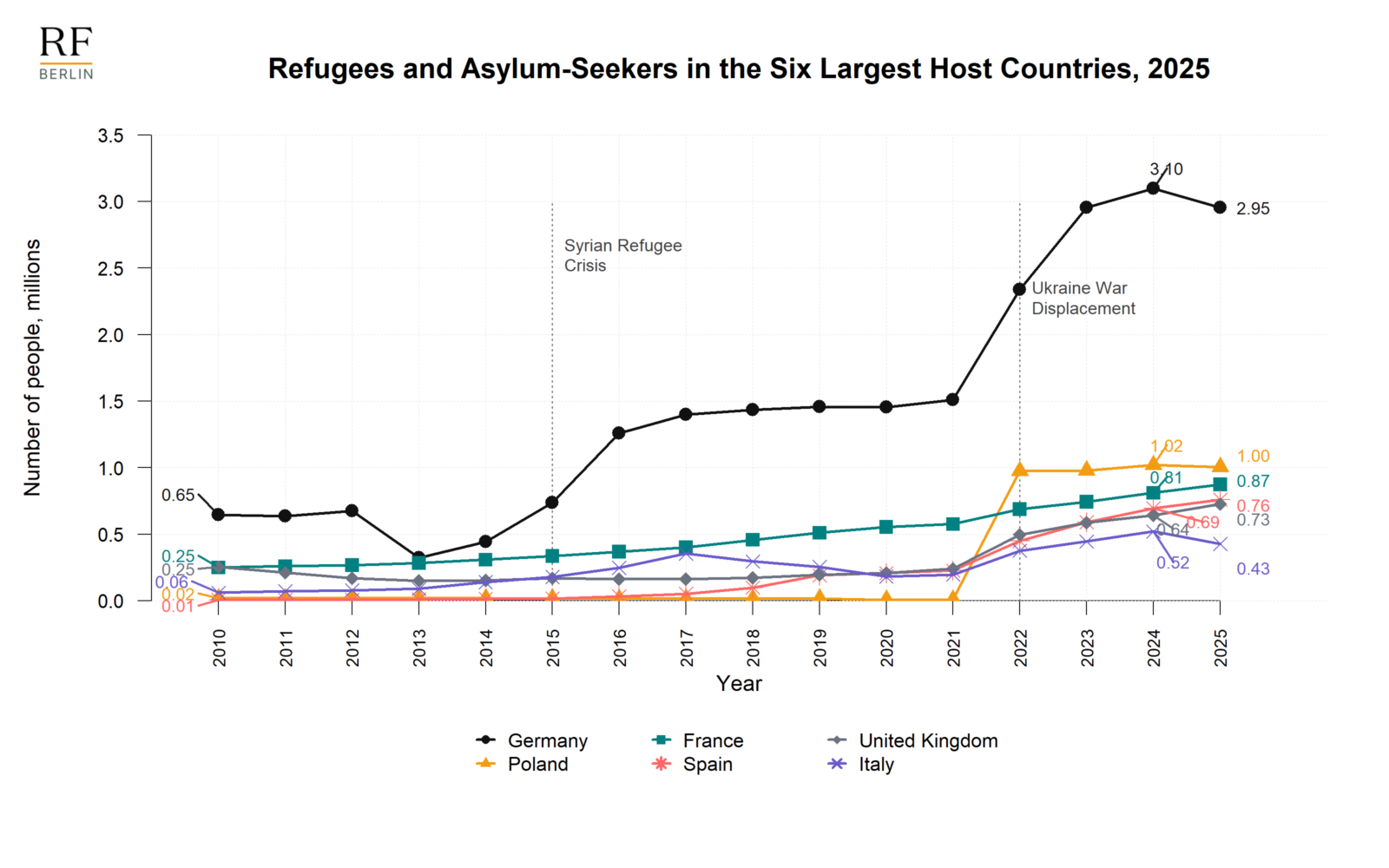

Germany has been the principal destination throughout the period (Figure 2), rising from 0.65 million refugees and asylum-seekers in 2010 to 2.95 million in 2025, with a peak of 3.10 million in 2024 (see Figure A.1 for number of refugees and asylum-seekers as a share of the country population). France, Spain and the United Kingdom instead expanded more gradually and Poland rose steeply after the 2022 invasion of Ukraine, to about 1.0 million. 2025 marks a turning point among the largest hosts: not only did Germany record a 4.7% decline in its stock of refugees and asylum seekers relative to the previous year, for the first time since 2013, but Poland also edged 1.5% lower than in 2024. The smaller destinations instead continued to grow in the same year, the United Kingdom by 13.3%, Spain by 9.6% and France by 7.8%. The slowdown is therefore concentrated in the two largest hosts, which are also those most affected by Ukrainian displacement. Italy is a special case: its combined stock fell from 0.52 million in 2024 to 0.43 million in 2025 (-17.9%), but as discussed in the following section, this decline stems almost entirely from a one-off administrative reconciliation of Italy’s Ukrainian temporary-protection register in mid-2025.

Figure 2

Source: UNHCR, (downloaded on 11 June 2026). Notes: End-year stocks of refugees and asylum-seekers in the six main European destination countries (Germany, Poland, France, Spain, the United Kingdom and Italy), 2010–2025, measured in millions. Refugees include persons granted refugee or related protection status; asylum-seekers are individuals whose claims have not yet been finally decided. Labels on the left report 2010 values; labels on the right report 2024 and 2025 values. Vertical dashed lines mark the Syrian refugee crisis (2015) and Russia’s invasion of Ukraine (2022).

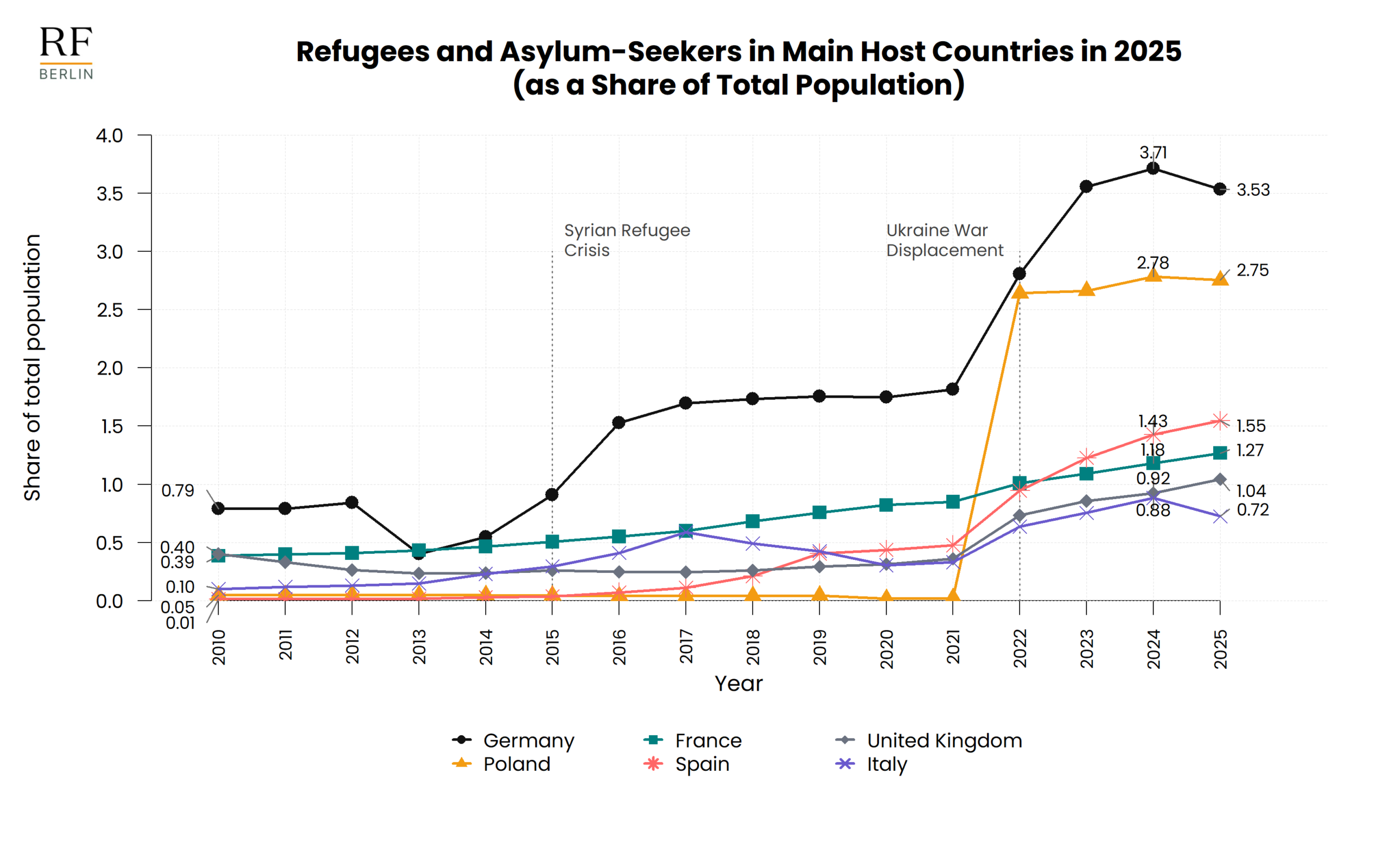

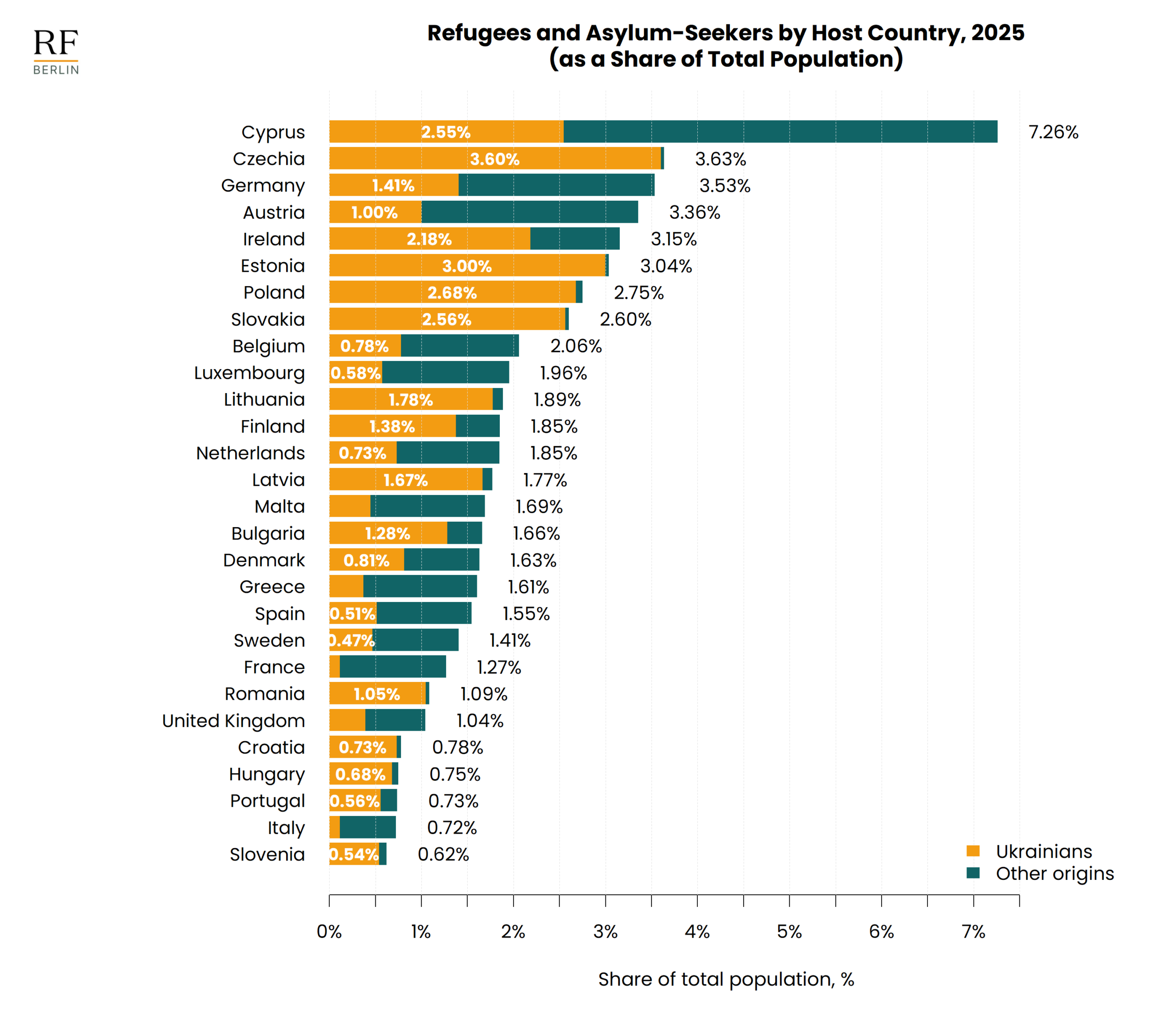

In 2025, Germany is by far the largest host country, with 2.95 million refugees and asylum-seekers, followed by Poland (1.00 million), France (0.87 million), Spain (0.76 million) and the United Kingdom (0.73 million). Germany ranks among the countries with the highest refugee and asylum-seeker populations, both in absolute terms and relative to population size. Refugees and asylum seekers account for 3.53% of Germany’s population, a share exceeded only by Cyprus (7.26%) and Czechia (3.67%). In contrast, France, the United Kingdom, and Italy have refugee and asylum-seeker shares below 1.3%, placing them below many smaller European countries (See Appendix Figure A.2).

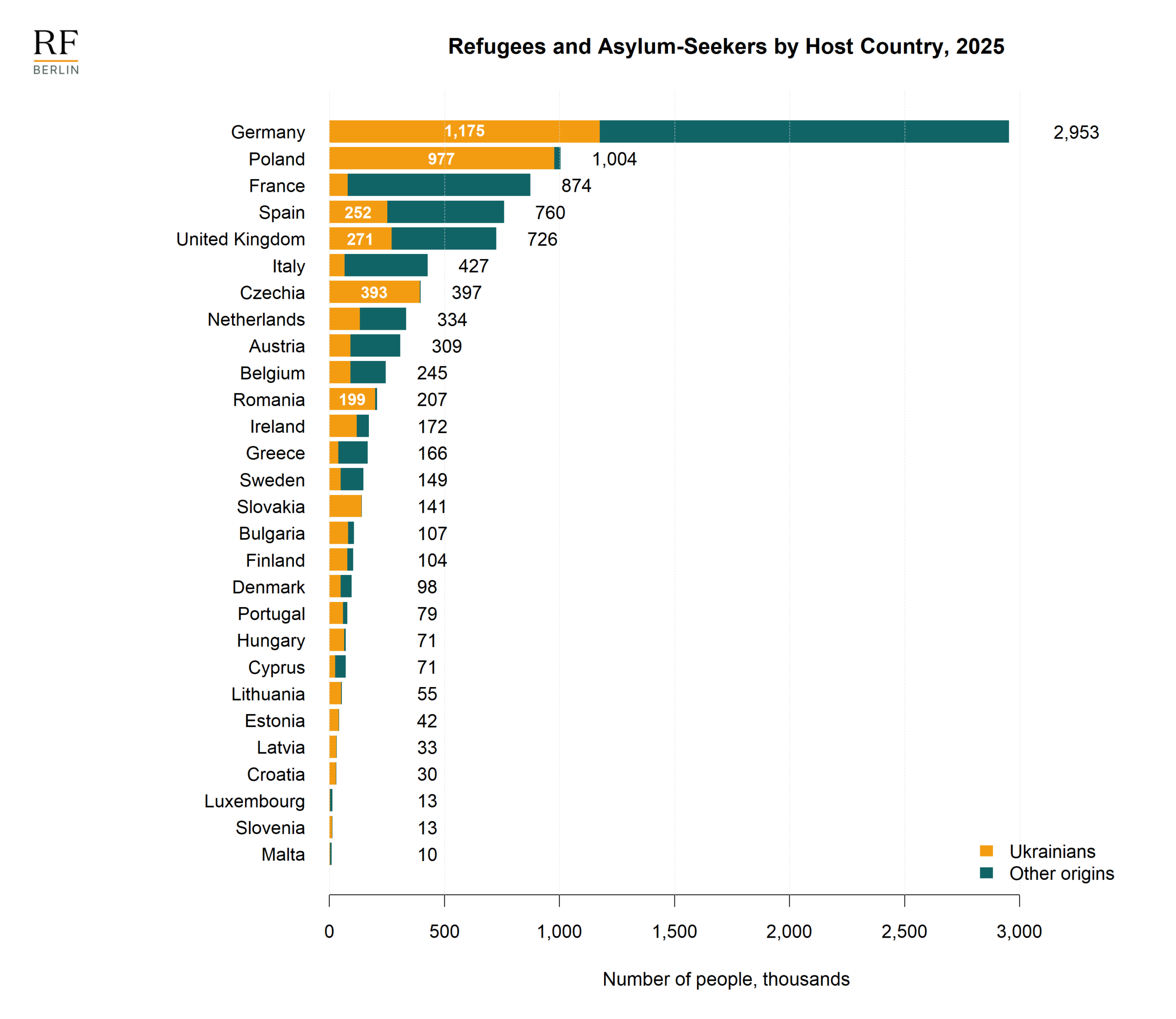

Figure 3 shows that the balance between Ukrainians and other origins varies sharply across hosts and closely follows geographic proximity to Ukraine. In Poland almost the entire population is Ukrainian (977,000 out of 1.00 million), as in neighbouring Czechia (393,000 out of 397,000) and Romania (199,000 out of 207,000). On the other hand, Germany, France, and the United Kingdom host more diverse populations: Ukrainians account for around 40% of the total in Germany (1.18 million), while in France and the United Kingdom, non-Ukrainians make up the vast majority of refugees and asylum seekers.

Figure 3

Source: UNHCR, (downloaded on 11 June 2026). Notes: Number of refugees under UNHCR’s mandate and asylum-seekers by host country, expressed in thousands of people. Refugees include individuals granted refugee status, complementary protection, temporary protection, and persons in refugee-like situations. Asylum-seekers are individuals whose asylum claims have not yet been finally decided. Bars are split between persons whose UNHCR country of origin is Ukraine and persons from all other origins. The total value shown at the end of each bar is the sum of both groups. The figure includes all EU27 member states as of February 1, 2020, plus the United Kingdom.

[1] UNHCR definition of refugees includes individuals granted complementary forms of protection, and those enjoying temporary protection. Ukrainian nationals residing in Ukraine until 24 February 2022, as well as third-country nationals residing in Ukraine on the basis of refugee status and who entered the EU after 24 February 2022 are granted Temporary Protection in EU according to the Temporary Protection Directive. Third-country nationals with permanent residence permits in Ukraine are also protected. The family members are also covered.

Asylum Applications Decline for Two Consecutive Years

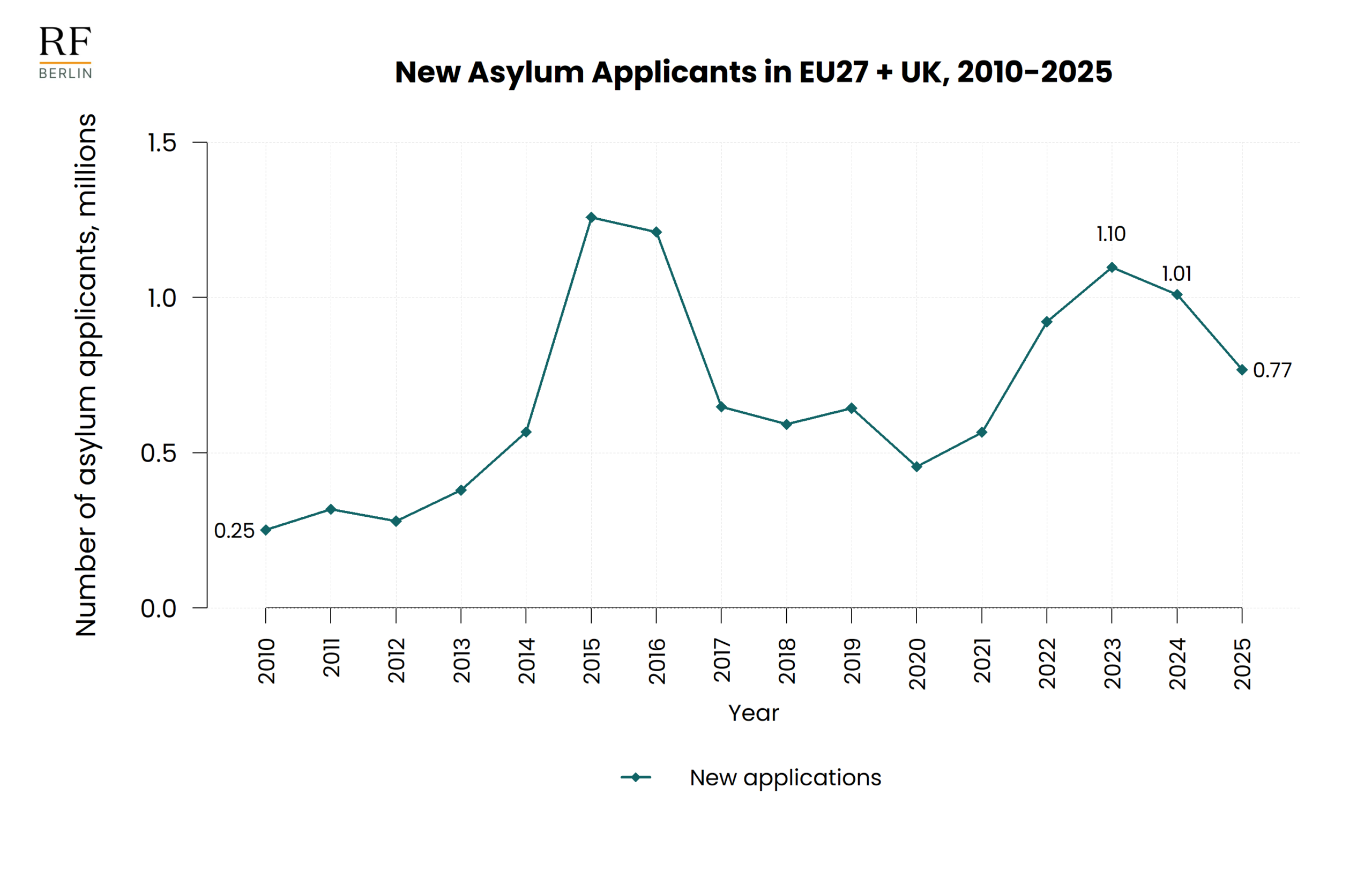

Asylum applications in the EU27 and the UK declined for a second consecutive year in 2025, falling by 23.8% to 770,000 claims. The decline was most pronounced in Germany, while other major destination countries experienced more moderate reductions. Falling applications from Syrian nationals – following the collapse of the Assad regime – accounted for most of the overall decrease, although Venezuelans became the largest single origin of new asylum applicants in 2025.

Asylum applications in Europe (EU27 + UK) have followed a pronounced cyclical pattern, peaking at 1.26 million during the 2015–2016 refugee crisis and again at 1.10 million in 2023. The 2025 update in Figure 4 sshows a second consecutive annual decline, with new applications falling by 23.8%, to 0.77 million.

Figure 4

Source: UNHCR, downloaded on 11 June 2026. Notes: Annual flows of first-time asylum applicants in the EU27 and the United Kingdom, expressed in millions of applicants. First-time applicants are persons who lodged an application for international protection for the first time in the reporting country; subsequent applicants are persons lodging a repeat application. Labels on the left report 2010 values; labels on the right report values for 2024 and 2025.

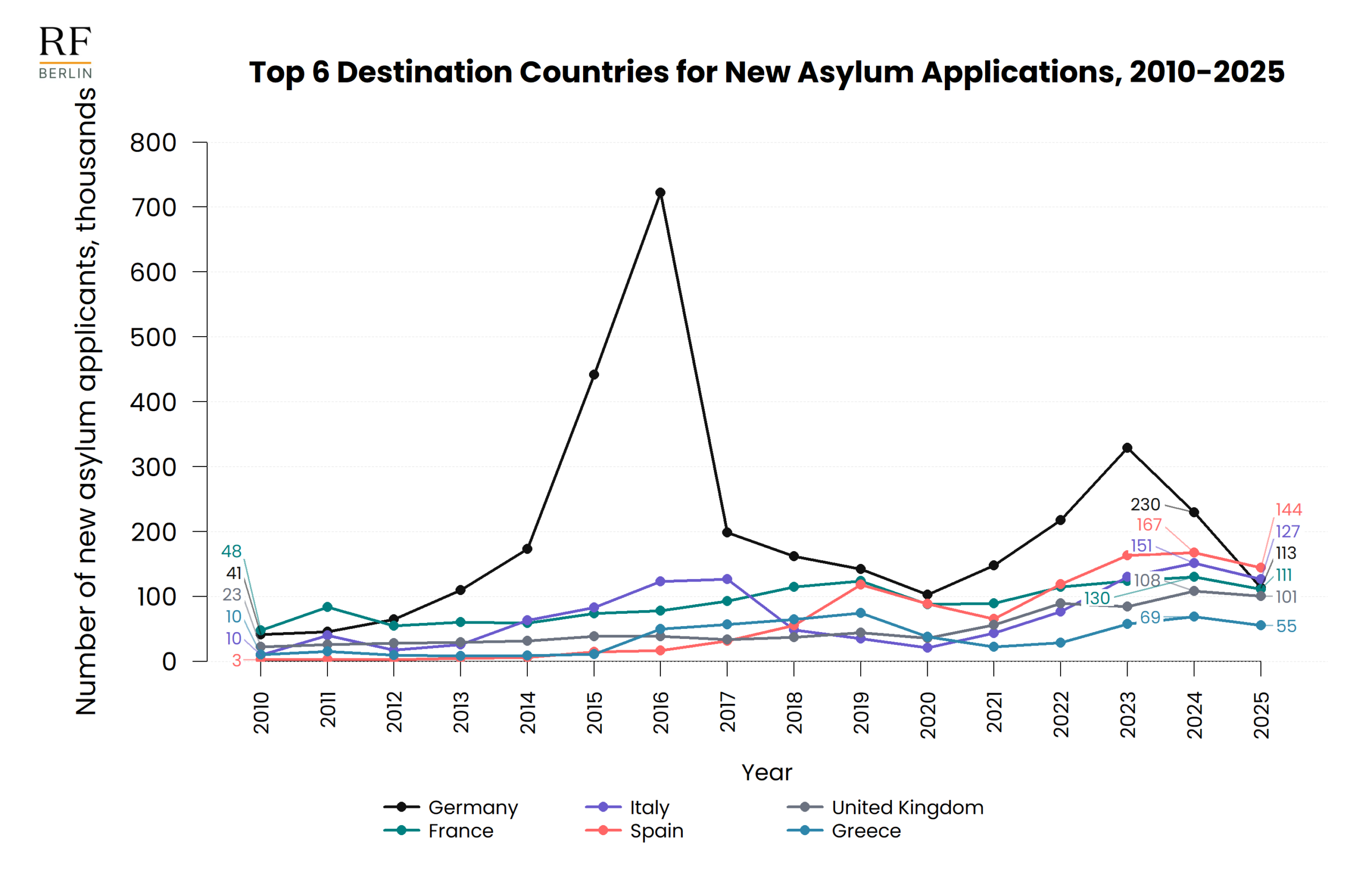

The aggregate EU+UK trend masks substantial differences across destination countries. Figure 5, therefore, shows the six countries with the highest number of asylum applicants over the period 2010-2025. Germany stands out as the dominant destination, especially during the 2015-2016 peak, and it remains the largest destination in 2025. However, Germany also records the sharpest recent decline among the top six countries, falling from around 230,000 new applicants in 2024 to around 113,000 in 2025. Germany’s increased border controls, introduced in October 2023 and intensified in 2025, may have contributed to this decline. These measures included turning back travellers without valid documents and extending temporary internal border controls within the Schengen area. Changes in push factors in origin countries, discussed below, likely also played a role. By contrast, France, Spain, Italy, and the United Kingdom show smaller declines over the same period.

Figure 5

Source: UNHCR, downloaded on 11 June 2026. Notes: Annual flows of first-time asylum applicants in the major destination countries, expressed in thousands of applicants. First-time applicants are persons who lodged an application for international protection for the first time in the reporting country. Labels on the left report 2010 values; labels on the right report values for 2024 and 2025.

The fall in applications is far from uniform across origins, and moving from a destination to an origin perspective clarifies what drives the aggregate decline. Table 1 reports the six largest origin countries of asylum applicants in the EU27 and the UK over 2021–2025. The 2025 contraction is concentrated in a few origins. Applications by Syrian nationals, the largest group for most of the period, collapsed from 148,000 in 2024 to 43,000 in 2025, a fall of more than 70%. This single drop accounts for the bulk of the decline in new applications and follows the collapse of the Assad regime in December 2024, which removed the principal push factor and led several European countries to pause the processing of Syrian claims. Afghan applications, the second-largest group, also fell, from 81,000 to 69,000 (-15%), alongside declines in applicants from Turkey (-46%), Colombia (-60%) and Bangladesh (-15%). Venezuela is the main exception: applications rose by 24%, to 91,000, making it the single largest origin of new applicants in 2025, with the vast majority of claims lodged in Spain, reflecting the continuing political and economic crisis there.

Table 1: Main origin countries of asylum applicants in the EU27 and the UK, 2021–2025

| Origin country | 2021 | 2022 | 2023 | 2024 | 2025 |

| Syria | 98,405 | 128,443 | 177,066 | 148,132 | 42,511 |

| Afghanistan | 78,017 | 112,317 | 106,099 | 81,214 | 69,201 |

| Venezuela | 17,607 | 50,565 | 67,564 | 73,417 | 90,683 |

| Turkey | 20,530 | 49,038 | 92,990 | 47,773 | 25,787 |

| Colombia | 13,453 | 42,760 | 63,704 | 52,587 | 21,263 |

| Bangladesh | 18,656 | 33,487 | 42,315 | 49,092 | 41,683 |

| Total (all origins) | 566,348 | 922,062 | 1,096,802 | 1,009,572 | 767,743 |

Source: UNHCR, downloaded on 11 June 2026; The table includes the six top origin countries by asylum applications over the period 2021-2025. The numbers represent new asylum applications submitted during the calendar year in the 27 EU member states (as of 1 February 2020) plus the United Kingdom. Values are annual application counts.

Explaining the Turnaround: Germany and Italy

As shown in Figure 2, Germany and Italy are the two major destination countries where the populations of refugees and asylum seekers decrease between 2024 and 2025. These declines offset increases in other destination countries, such that the total population in the EU27 and the UK stabilizes in 2025. The declines in these two countries are due to different factors, which we discuss in this section.

The Decline of Refugee and Asylum Seekers Population in Germany

Germany’s refugee and asylum-seeker population declined in 2025 as both refugee stocks and new asylum applications fell across several major origin groups. However, the decline was driven primarily by naturalisation rather than by refugees leaving the country. Among Syrians and Iraqis, who account for most of the non-Ukrainian decline, new German citizenship acquisitions greatly exceeded assisted returns, indicating that integration and status transitions played a much larger role than return migration.

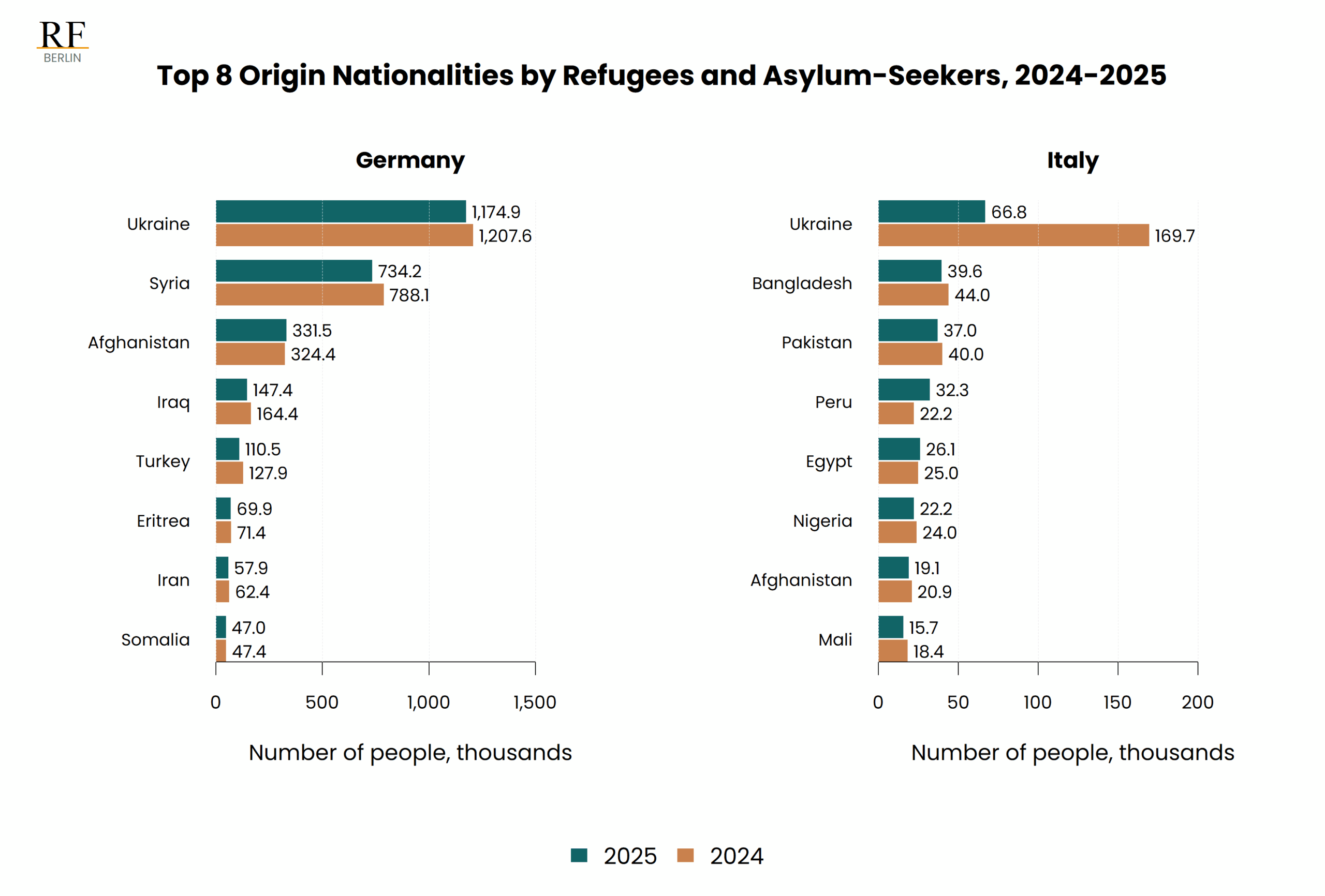

Germany recorded a clear decline in its refugee and asylum-seeker population in 2025. As shown in Figure 6, the total number of refugees and asylum-seekers from the main origin groups fell for several large populations, most visibly Syrians, Iraqis, Turks and Ukrainians. The Syrian stock declined from 788,100 in 2024 to 734,200 in 2025, while the Iraqi stock fell from 164,400 to 147,400. Ukraine remained by far the largest origin group in Germany, but also declined slightly, from 1.21 million to 1.17 million. Afghan nationals were the main exception, increasing from 324,400 to 331,500.

Figure 6

Source: UNHCR, downloaded on 11 June 2026. Notes: The figure shows the main countries of origin among refugees under UNHCR’s mandate and asylum-seekers in Germany and Italy in 2024 and 2025, expressed in thousands of people. Values refer to destination-country stocks and do not measure new arrivals or asylum applications. Refugees include individuals granted refugee status, complementary protection, temporary protection, and persons in refugee-like situations. Asylum-seekers are individuals whose asylum claims have not yet been finally decided.

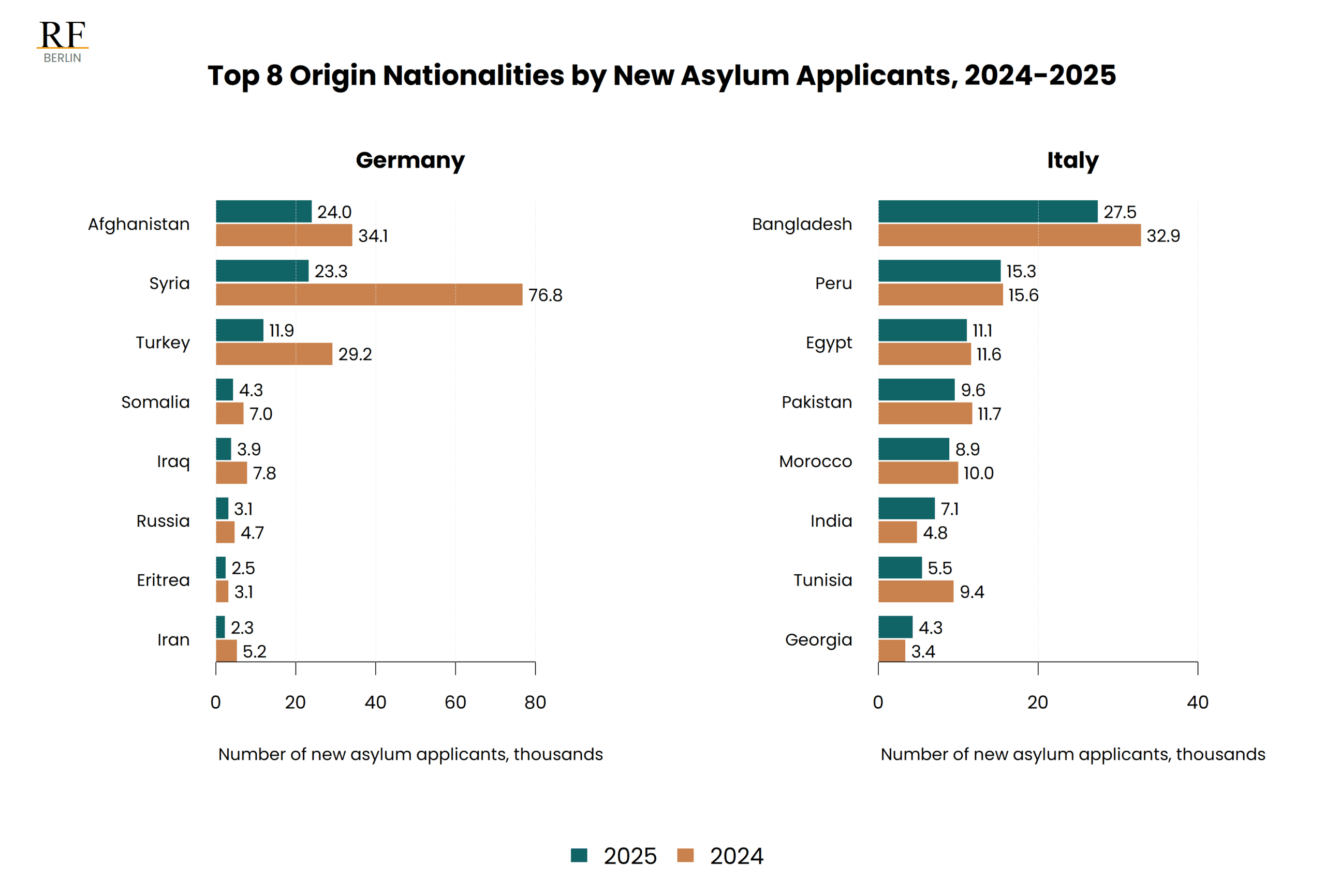

Figure 7 shows that the stock decline took place alongside a sharp fall in new asylum applications from several of the same origin groups. Applications by Afghans decreased from 34,100 in 2024 to 24,000 in 2025. Syrian new applicants fell from 76,800 in 2024 to 23,300 in 2025, while applications by Iraqis declined from 7,800 to 3,900 and applications by Turkish nationals from 29,200 to 11,900. This fall in applications is an important part of the explanation: fewer new arrivals and fewer new claims reduced the inflow into the refugee and asylum-seeker population.

Figure 7

Source: UNHCR, downloaded on 11 June 2026. Notes: The figure shows the main countries of origin among new asylum applicants in Germany and Italy in 2024 and 2025, expressed in thousands of people.

Table 2 provides a decomposition of the change in the population of Syrian and Iraqis refugees and asylum seekers in Germany between 2024 and 2025. Together these origin countries account for about 61% of the decrease in the non-Ukrainian population of refugees and asylum seekers in Germany.[2] We decompose the change in stock into the sum of four components: new inflows, naturalisations, assisted voluntary returns under Reintegration and Emigration Programme for Asylum Seekers in Germany and Government Assisted Repatriation Programme (REAG/GARP), and a residual “Other” category capturing status changes, onward migration, deaths, and differences in statistical coverage see Technical Appendix for details).

Table 2: Decomposition of the change in the refugee and asylum-seeker stock in Germany, 2024–2025

| Origin group | Population 2024 |

Population 2025 |

Change | Inflows | Naturalisations | REAG/GARP Returns | Other |

| Syrians | 788,061 | 734,158 | −53,903 | + 23,256 | −65,574 | −3,678 | −7,907 |

| Iraqis | 164,440 | 147,415 | −17,025 | + 3,860 | −13,750 | −849 | −6,286 |

Source: UNHCR, downloaded on 11 June 2026. Decomposition of the change in the population of Syrian and Iraqis refugees and asylum seekers in Germany between 2024 and 2025 in number of persons. The Identity: Population 2025 = Population 2024 + Inflows − Naturalisations − Returns – Other transitions. Inflows are new asylum applications filed during the year. Naturalisations refer to all nationals of the group, not only refugees. Returns capture assisted voluntary returns under the REAG/GARP programme. Other is the residual required to reconcile the identity and includes status changes, onward migration, deaths, and other unobserved flows. A negative value is an additional net outflow; a positive value an additional net inflow.

For Syrians, the refugee and asylum-seeker population declined by almost 54,000 between 2024 and 2025, despite more than 23,000 new asylum applications during the year. The primary reason was naturalisation. In 2025, more than 65,000 Syrian nationals acquired German citizenship – more than the total decline in the Syrian refugee population. In other words, many individuals who had arrived as refugees in earlier years remained in Germany but were no longer counted as refugees after becoming German citizens. Assisted voluntary returns accounted for only a small share of the decline, as did other factors such as independent returns and onward migration.

A similar pattern is evident among Iraqis. The refugee and asylum-seeker population fell by around 17,000, while almost 14,000 Iraqi nationals acquired German citizenship. Returns again played only a minor role.

These figures suggest that the decline in Germany’s refugee and asylum-seeker population in 2025 was driven primarily by naturalisation rather than by refugees leaving the country. It reflects the gradual integration of earlier refugee cohorts, many of whom had accumulated sufficient residence, language skills, economic self-sufficiency, and civic knowledge to qualify for German citizenship. Lower inflows than in previous years reinforced this trend, but naturalisation was by far the most important factor behind the decline. [3]

[2] Ukrainians are a special case because most fall under temporary protection rather than the asylum system, and their displacement follows a distinct migration pathway. According to UNHCR estimates based on IOM’s Returns Report — General Population Survey and Internal Displacement Report — General Population Survey (Round 22, December 2025), 26,000 returns from Germany in 2025, explaining a large share of the decline in the Ukrainian population between 2024 and 2025. Among non-Ukrainian asylum-related populations, by contrast, the largest declines were observed for Syrians and Iraqis.

[3] A caveat is that the naturalisation figures cover all nationals from each origin country rather than only former refugees. However, given the magnitude and timing of Syrian and Iraqi naturalisations, it is likely that the vast majority of naturalised Syrians and Iraqis are former refugees.

The Decline of Refugee and Asylum Seekers Population in Italy

Italy’s refugee and asylum-seeker population fell sharply in 2025, but the decline was almost entirely driven by the administrative removal of Ukrainians from the temporary-protection register following a new permit-renewal procedure. The drop should therefore be interpreted primarily as a statistical correction, not as evidence of a sudden reduction in the protected population present in Italy.

Italy is the second major host country to record a substantial decline in its refugee and asylum-seeker population in 2025. The total fell from 520,100 in 2024 to 427,100 in 2025, a reduction of about 93,000 people (-17.9%), as shown in Figure 2. Unlike Germany, however, this decline does not reflect fewer asylum claims or a shrinking asylum system. In fact, the number of asylum seekers with a pending application increased from 207,300 to 234,100 (+26,900). The decline is entirely driven by a sharp fall in the number of recognised refugees, which dropped from 312,800 to 192,900 (-119,900). Almost all of this decline is accounted for by Ukrainians under temporary protection. Their recorded number fell from 167,800 in 2024 to 64,700 in 2025, a reduction of 103,100 people (Figure 6, right panel). This change alone is larger than the overall decline in Italy’s refugee and asylum-seeker population.

This decline is largely the consequence of a change in Italian legislation about refugees under temporary protection. At the end of 2024, Italy reformed its temporary protection regime through Article 20 of Decree-Law 202/2024, effective in 2025. The decree introduced several changes in the system. First, it replaced the automatic extension of temporary protection permits with a renewal procedure requiring beneficiaries to apply actively at the police headquarters, while extending protection first to 4 March 2026 and later to 4 March 2027. At renewal, holders may also convert their permit into an ordinary residence permit for work. Second, it reduced the scope of the extraordinary assistance regime put in place after 2022. The cash subsistence contribution was discontinued for permits issued after February 2025, funding for the dedicated emergency reception system was provided only until the end of 2025 before beneficiaries were transferred to the ordinary reception system, and enrolment in the national health service was guaranteed through the same date.

Among these reforms, the new renewal requirement appears to have had the most immediate impact on the recorded number of beneficiaries under temporary protection. The sharp fall recorded in 2025 is a direct consequence of this change and should be read as a statistical correction rather than a sudden departure of Ukrainians from Italy[4]. Monthly Eurostat data show that the number of Ukrainians registered under temporary protection remained broadly stable at around 165,000 from late 2023 through May 2025, then fell almost entirely in June 2025, to 41,200. Until then, beneficiaries were generally removed from the register only if they formally notified the authorities that they had left the country, so the register gradually accumulated permits belonging to people who had already moved elsewhere or were no longer using temporary protection in Italy. When the new renewal procedure came into force, individuals who did not renew were removed in June 2025. It is possible that part of the roughly 100,000 permits cancelled belonged to people who had already left the Italian temporary-protection system in earlier years, either by moving to another EU country or by returning to Ukraine. Italy’s 2025 decline should therefore be interpreted primarily as a reconciliation of the temporary protection register.

The provisions of the reform are likely to prevent the recorded Ukrainian population in Italy from growing significantly in the coming years. The end of the subsistence contribution and the gradual phase-out of dedicated emergency reception reduce the support attached to temporary-protection status, weakening the incentive to register or to maintain it, while the option to convert to a work permit moves settled beneficiaries out of the temporary-protection count altogether.

[4] See data-break explanation on Eurostat.

Conclusion

The refugee and asylum-seeker population in the EU27 and the UK remains historically high, but the rapid growth following Russia’s invasion of Ukraine appears to have come to an end. In 2025, the aggregate stock was broadly stable, while new asylum applications declined for a second consecutive year. This stability masked substantial cross-country differences: declines in Germany and Italy were offset by continued growth in France, Spain, and the United Kingdom. Absent a new conflict at Europe’s borders or another major displacement shock, these trends are likely to persist. Refugee populations may remain large, but future developments will increasingly be shaped by naturalisations, status changes, returns, and administrative adjustments rather than by large new inflows.

Germany illustrates this shift particularly clearly. The decline in its refugee and asylum-seeker population in 2025 was driven primarily by lower inflows and the movement of earlier refugee cohorts – especially Syrians and Iraqis – out of refugee statistics through naturalisation and other status changes, rather than by large-scale departures. Italy reinforces the same point from a different angle: its apparent decline largely reflects a reconciliation of the temporary protection register for Ukrainians rather than a sudden substantial reduction in the protected population residing in the country. Looking ahead, the broader reform of temporary protection in Italy is likely to hold this number broadly stable rather than allow it to resume growing. Together, these cases show that changes in refugee stocks cannot be interpreted solely as changes in arrivals and departures; integration policies, naturalisation rules, and administrative practices also play an important role.

The outlook depends heavily on developments in Ukraine. In 2025, Ukrainians account for almost half of the refugee and asylum-seeker population in the EU27 and the United Kingdom, largely under temporary protection. A large-scale return to Ukraine or changes in temporary-protection arrangements could therefore substantially reduce Europe’s recorded refugee population. At the same time, the EU Pact on Migration and Asylum, which enters into application in 2026, is likely to strengthen border screening, asylum procedures, returns, and cooperation with third countries. While these policies may help contain future inflows, the principal source of uncertainty remains geopolitical: a new major conflict near Europe could quickly reverse the current stabilization.

Technical Appendix

The decomposition analysis relies on the following datasets:

1. Population in 2024 and 2025: Stock of refugees under UNHCR’s mandate and asylum seekers, UNHCR Population figures dataset, downloaded on 11 June 2026. This dataset is used to construct the population figures for Syrians and Iraqis reported in Table 2.

2. Inflows: New asylum applications, UNHCR Asylum applications dataset, downloaded on 11 June 2026. This dataset is used to construct the new inflow figures for Syrians and Iraqis reported in Table 2.

3. Naturalisations: New naturalisations of foreigners, DESTASIS Naturalisation statistics dataset, downloaded on 17 June 2026. This dataset is used to construct the naturalisations figures for Syrians and Iraqis reported in Table 2. The statistics cover all Syrian and Iraqi nationals naturalised in Germany and do not distinguish between refugees and individuals holding other residence statuses. We therefore assume that the majority of naturalised individuals hold a refugee status.

REAG/GARP returns: Returns in 2025 supported through the REAG/GARP programme, Returnees’ most common destination countries, BAMF – Bundesamt für Migration und Flüchtlinge – Voluntary return, accessed on 17 June 2026. This data source is used to construct the return figures to Syria and Iraq in Table 2. The statistics refer to the number of individuals returning to Syria and Iraq as destination countries but do not report the nationality of returnees. We therefore assume that the majority of individuals returning to Syria and Iraq are Syrian and Iraqi nationals, respectively.

Appendix A

Figure A.1

Source: UNHCR, downloaded on 11 June 2026; Eurostat migr_pop3ctb; UK ONS. Notes: The figure reports annual number of refugees under UNHCR’s mandate and asylum-seekers in the six main destination countries in 2025, expressed as a share of each host country’s total population. Values combine refugees and asylum-seekers and refer to destination-country stocks, not new arrivals or asylum applications. Refugees include individuals granted refugee status, complementary protection, temporary protection, and persons in refugee-like situations. Asylum-seekers are individuals whose asylum claims have not yet been finally decided. The temporary decline in 2013 reflects a change in Germany’s reporting methodology.

Figure A.2

Source: UNHCR, downloaded on 11 June 2026; Eurostat migr_pop3ctb; UK ONS. Notes: The figure reports 2025 number of refugees under UNHCR’s mandate and asylum-seekers by host country, expressed as a share of each host country’s total population. Refugees include individuals granted refugee status, complementary protection, temporary protection, and persons in refugee-like situations. Asylum-seekers are individuals whose asylum claims have not yet been finally decided. The temporary decline in 2013 reflects a change in Germany’s reporting methodology.